Why California painters need insurance: liability and coverage

- Jonathan Hernandez

- Mar 20

- 10 min read

Many painters believe their work carries minimal risk and skip insurance to save money. Yet a single spill, ladder fall, or overspray incident can trigger lawsuits costing tens of thousands of dollars. California regulations now mandate specific insurance types even for solo painting contractors, making coverage both a legal requirement and a financial safeguard. Understanding liability and workers’ compensation insurance protects your business from devastating claims while opening doors to better contracts and long-term growth.

Table of Contents

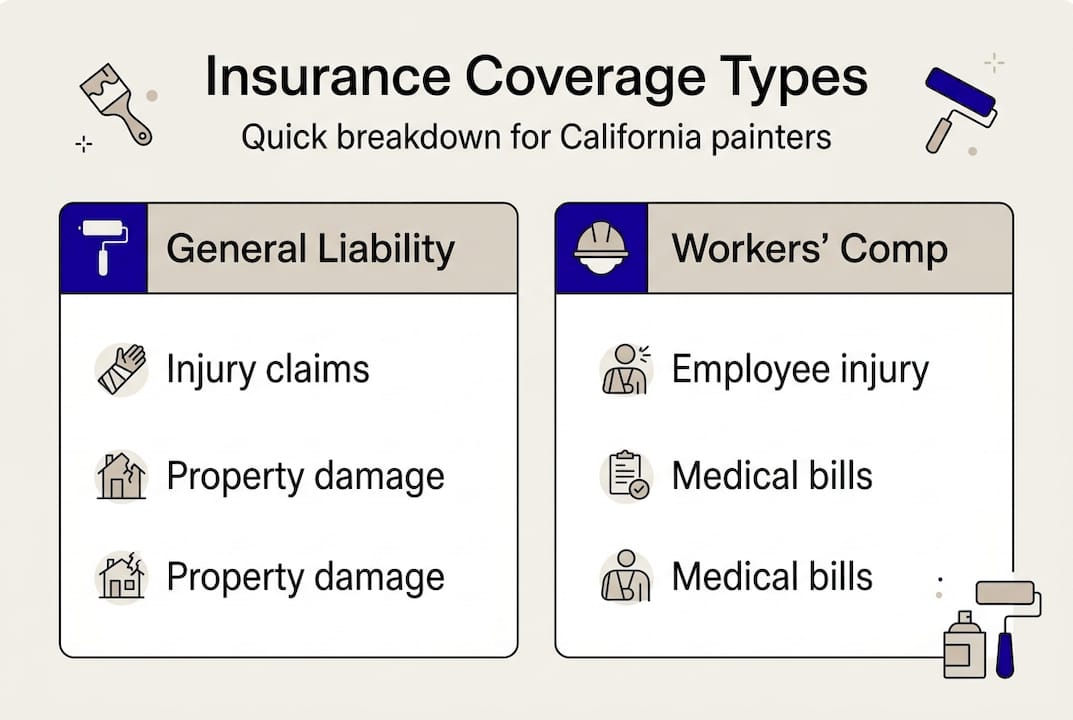

Why general liability insurance is a must for California painters

Understanding workers’ compensation insurance requirements and costs

Navigating special insurance considerations for California painting contractors

Real-life insurance claims and risk management tips for painters

Protect your painting business with the right insurance and expert support

Key Takeaways

Point | Details |

General liability required | California requires licensed painters to carry general liability insurance to cover third party claims from spills and property damage. |

Pollution liability add on | Standard general liability policies often exclude chemical spills and lead paint exposure, so add pollution liability to cover environmental cleanup. |

Workers’ comp mandatory 2026 | California requires all licensed C-33 painters to carry workers’ compensation even if they work solo. |

Payroll based premiums | Workers’ compensation premiums depend on payroll and classification code 5474, with 2026 rates ranging from 7.98 to 8.83 per $100 of payroll for standard painting and higher for high risk work. |

Why general liability insurance is a must for California painters

General liability insurance serves as your first line of defense against claims from clients, property owners, and third parties. This coverage protects you when paint spills damage furniture, ladders knock over expensive fixtures, or overspray ruins landscaping. It also handles legal defense costs if a homeowner slips on your drop cloth and files a bodily injury lawsuit. Without this protection, you pay these expenses out of pocket, which can bankrupt a small painting business.

California’s Contractors State License Board requires all licensed painters to maintain general liability coverage. The recommended minimum sits at $1 million per occurrence and $2 million aggregate, though many commercial clients demand $5 million limits before they’ll even consider your bid. These higher limits signal financial stability and professionalism, making you more competitive for lucrative contracts.

Pollution liability deserves special attention in California’s strict environmental regulatory climate. Standard general liability policies often exclude coverage for chemical spills, solvent vapors, and lead paint contamination. Adding pollution liability endorsements protects you when paint thinners seep into soil, VOC emissions trigger neighbor complaints, or improper lead paint handling violates EPA standards. This coverage typically costs an additional $500 to $1,200 annually but shields you from cleanup costs that can exceed $50,000.

Pro Tip: Request certificates of insurance from any subcontractors you hire. If their coverage lapses and they cause damage, your policy becomes the primary target for claims.

Most general contractors and property management companies maintain strict contractor insurance requirements as part of their vendor qualification process. You’ll need to provide current certificates naming them as additional insureds, proving your coverage meets their specifications. Failing this step disqualifies you from bidding, regardless of your skills or competitive pricing.

Understanding what general liability does not cover is equally important. Employee injuries fall outside GL protection entirely. Tool theft, equipment breakdown, and your own medical bills require separate policies. Liability coverage benefits extend only to third-party claims, so structure your insurance portfolio accordingly.

Understanding workers’ compensation insurance requirements and costs

California implemented sweeping changes to workers’ compensation requirements in 2026, eliminating previous exemptions for sole proprietors. Now all licensed C-33 painters must carry workers’ comp coverage, even if they work alone without employees. This mandate aims to protect painters from catastrophic medical bills and lost wages following workplace injuries while standardizing coverage across the industry.

Workers’ compensation premiums calculate based on your payroll and classification code. California assigns painters to code 5474, which carriers use to determine your rate per $100 of payroll. These rates fluctuate based on claim history within the painting industry statewide. For 2026, rates range from $7.98 to $8.83 per $100 of payroll for standard painting work, though high-risk activities like industrial coating can push rates to $38.66.

Consider a practical example. A painting contractor with $40,000 in annual payroll at the standard rate of $8.50 per $100 would pay approximately $3,400 yearly, or roughly $283 monthly. Adding a second employee doubles the payroll and the premium. These costs represent baseline estimates before applying experience modification factors or safety credits that can adjust your final premium up or down.

Pro Tip: Pay workers as W-2 employees rather than 1099 contractors. Misclassification triggers audits, back premiums, and penalties that often exceed three times the original premium amount.

The consequences of operating without workers’ compensation extend beyond fines. California imposes penalties of $10,000 per employee for each violation, plus potential criminal charges for willful non-compliance. The Contractors State License Board can suspend or revoke your C-33 license, effectively shutting down your business. If an uninsured employee suffers a serious injury, you face unlimited personal liability since you lose the protections that workers’ comp provides against employee lawsuits.

Understanding the coverage distinctions between workers’ compensation and general liability prevents dangerous gaps in protection. Workers’ comp handles employee medical bills, rehabilitation costs, disability payments, and death benefits. General liability covers third parties like clients and visitors. Neither policy substitutes for the other, making both essential for comprehensive protection.

Payroll amount | Monthly premium estimate | Annual premium estimate |

$20,000 | $142 | $1,700 |

$40,000 | $283 | $3,400 |

$60,000 | $425 | $5,100 |

$80,000 | $567 | $6,800 |

$100,000 | $708 | $8,500 |

Exploring workers’ compensation benefits helps you understand what this mandatory coverage delivers beyond legal compliance. Injured employees receive prompt medical care without filing lawsuits, protecting your business relationships and reputation. The coverage also includes employer’s liability insurance, defending you against claims that fall outside standard workers’ comp protections.

Navigating special insurance considerations for California painting contractors

Lead paint regulations create unique insurance and certification requirements for California painters. Any renovation, repair, or painting work on homes built before 1978 requires EPA RRP certification, which costs approximately $300 and renews every five years. This certification mandates specific containment, cleanup, and disposal procedures when disturbing lead-based paint. Your general liability policy should include lead paint coverage, as standard pollution exclusions might deny claims from improper lead abatement.

Pollution liability becomes critical when your work involves solvents, chemical strippers, or spray applications. Solvent spills and chemical releases trigger environmental cleanup obligations that can reach six figures. Standard general liability policies exclude pollution events, requiring separate pollution liability coverage or specific endorsements. California’s strict environmental laws impose cleanup costs on responsible parties regardless of intent, making this coverage non-negotiable for contractors using hazardous materials.

Height classifications significantly impact workers’ compensation premiums. California splits painting work into different classification codes based on elevation. Code 5474 covers standard painting, while code 5037 applies to work exceeding two stories or requiring scaffolding and rigging. The higher-risk classification carries substantially increased rates, sometimes doubling your workers’ comp costs. Accurately reporting the percentage of time spent at various heights prevents audit surprises and ensures proper coverage.

Pro Tip: Document every job’s height requirements with photos and project specifications. This evidence protects you during workers’ comp audits when carriers challenge your classification splits.

Obtaining your C-33 painting contractor license requires posting a $25,000 contractor license bond with the Contractors State License Board. This bond protects consumers from license law violations, contract breaches, and unpaid bills. While not insurance in the traditional sense, the bond represents a financial guarantee that you’ll operate ethically. Bond claims damage your ability to secure future bonds and can result in license suspension.

Understanding coverage gaps prevents costly mistakes. General liability does not protect your tools, equipment, or vehicles. A comprehensive business insurance portfolio includes:

Inland marine coverage for tools and equipment, whether stored at your shop or transported to job sites

Commercial auto insurance for vehicles used in business operations, as personal auto policies exclude commercial use

Business property coverage for your office, warehouse, or storage facility

Professional liability insurance if you provide color consulting or design services beyond basic painting

Coverage type | What it protects | What it excludes |

General liability | Client injury, property damage, legal defense | Employee injuries, tools, pollution (without endorsement) |

Workers’ compensation | Employee medical bills, disability, death benefits | Third-party claims, tools, vehicles |

Pollution liability | Chemical spills, environmental cleanup, lead contamination | Intentional violations, employee exposure claims |

Inland marine | Tools, equipment, materials in transit | Wear and tear, employee theft |

Exploring home transformation safety practices demonstrates how proper project management reduces insurance claims. Implementing systematic safety protocols protects both your team and clients while demonstrating the professionalism that insurance carriers reward with lower premiums.

Many painters overlook the distinction between occurrence-based and claims-made policies. Occurrence policies cover incidents that happen during the policy period, regardless of when claims are filed. Claims-made policies only respond if both the incident and claim filing occur while coverage is active. For painting contractors, occurrence-based general liability provides superior protection since property damage or injury might not surface until months or years after project completion. Understanding these policy structures prevents coverage gaps when switching carriers or retiring from business. Review the complete insurance guide for deeper insights into policy structures and coverage options.

Real-life insurance claims and risk management tips for painters

Actual insurance claims illustrate the financial devastation painters face without proper coverage. One California painter spilled paint remover on a client’s hardwood floors, damaging the finish throughout a 2,000-square-foot living area. The restoration required complete floor refinishing at $8,500, plus the client’s damaged furniture replacement costing $4,200. Including the general contractor’s markup and project delays, the total claim reached $34,700. General liability insurance covered the entire amount, saving the contractor from bankruptcy.

Another case demonstrates how claims can exceed standard coverage limits. A California painter’s employee caused a multi-vehicle accident while driving to a job site, resulting in severe injuries to three people. The resulting lawsuit produced a $5.3 million settlement that exceeded the contractor’s $1 million general liability limit. The painter faced personal asset seizure to cover the difference, losing his home and retirement savings. This case highlights why many contractors now carry umbrella policies providing $5 million to $10 million in additional coverage above their primary limits.

Proper worker classification serves as your first defense against premium increases and audit penalties. Insurance carriers audit payroll records annually, comparing your reported classifications against actual work performed. Misclassifying high-risk work as standard painting triggers retroactive premium charges, penalties, and potential fraud investigations. Maintaining detailed job records showing work locations, heights, and activities provides documentation supporting your classifications.

Your experience modification factor, or mod, directly impacts workers’ compensation premiums. This number compares your claim history to other painting contractors of similar size. A mod of 1.0 represents average risk, while 0.8 indicates 20 percent better safety performance and earns a 20 percent premium discount. Conversely, a 1.5 mod adds 50 percent to your base premium. Implementing aggressive safety programs and promptly addressing minor injuries before they become claims keeps your mod low and premiums manageable.

Pro Tip: Challenge every workers’ comp claim coding error immediately. A single claim miscoded as lost-time instead of medical-only can inflate your mod for three years, costing thousands in unnecessary premiums.

Implementing systematic safety practices reduces both claim frequency and severity:

Conduct daily toolbox talks addressing specific hazards for each job site

Require fall protection equipment for any work above six feet, exceeding OSHA’s ten-foot standard

Implement a return-to-work program offering light duty for injured employees, reducing lost-time claims

Document all safety training with signed acknowledgments protecting you from negligence claims

Perform monthly vehicle inspections and maintain driver qualification files

California’s Division of Occupational Safety and Health conducts random inspections of painting contractors, particularly on commercial and multi-family projects. Citations for safety violations average $7,000 to $25,000 and trigger increased workers’ comp audits. Maintaining OSHA compliance protects your insurance rates while demonstrating the professionalism that attracts premium clients.

Misclassification extends beyond workers to how you categorize your business operations. Describing your services as “residential repainting” versus “industrial coating” dramatically affects premium calculations. Be honest but strategic in how you present your work to insurance carriers. Specialize in lower-risk residential projects when possible, subcontracting high-risk industrial work to specialists with appropriate coverage and experience.

Reviewing expert painting safety protocols provides actionable strategies for reducing workplace hazards. These practices protect your team while building the safety record that insurance carriers reward with preferred rates and better coverage terms. Understanding risk management essentials helps you identify and address vulnerabilities before they trigger claims.

“Insurance exists to transfer risk you cannot afford to retain. Every painter faces catastrophic loss potential from a single incident. The question isn’t whether you can afford insurance, but whether you can survive without it.”

Protect your painting business with the right insurance and expert support

Navigating California’s complex insurance requirements while running a successful painting business demands expertise and reliable resources. Johnny’s Custom Painting brings over 16 years of industry experience to Los Angeles, combining superior craftsmanship with comprehensive insurance knowledge and strict safety protocols. Our licensed and insured status demonstrates the professional standards that protect both our business and our clients.

Explore our insurance information resources to understand how proper coverage protects your painting business while meeting California’s legal requirements. Review our interior residential painting portfolio showcasing completed projects that reflect our commitment to quality and safety. Whether you’re establishing your painting business or expanding your operations, Johnny’s Custom Painting provides the expertise and guidance you need to build a protected, profitable enterprise in California’s competitive market.

Frequently asked questions

Do painters in California need general liability insurance?

Yes, California law requires all licensed painters to carry general liability insurance with minimum coverage of $1 million per occurrence and $2 million aggregate. Most clients and general contractors demand proof of insurance before awarding contracts, making this coverage essential for both legal compliance and business development.

Is workers’ compensation insurance mandatory for sole proprietor painters in California?

Starting in 2026, all licensed C-33 painters in California must carry workers’ compensation insurance, including sole proprietors operating without employees. This regulation eliminates previous exemptions, ensuring all painting professionals have protection against workplace injuries and medical expenses. Operating without coverage results in license suspension and penalties exceeding $10,000 per violation.

What risks does general liability insurance cover for painters?

General liability insurance protects painters against third-party bodily injury claims, property damage from spills or accidents, legal defense costs, and pollution liability related to chemical exposure or environmental contamination. This coverage does not extend to employee injuries, stolen tools, or vehicle accidents, which require separate workers’ compensation, inland marine, and commercial auto policies.

How can painters reduce their insurance premiums in California?

Properly classify employees under California code 5474 to avoid audit penalties and premium surcharges that can double your costs. Implement comprehensive safety protocols including daily toolbox talks, fall protection requirements, and return-to-work programs to reduce claim frequency. Maintain a low experience modification factor through aggressive claims management, earning premium discounts of 20 to 50 percent. Review safety protocols and transformation practices to identify additional risk reduction strategies that lower your insurance costs while protecting your team.

Recommended

Comments